Executive summary

Jun 15, 2026

4 min to read

While some unforeseen circumstances are unavoidable, selling a business should not be a leap into the unknown for an entrepreneur who is prepared. Yet, it is common for entrepreneurs to approach a sale process feeling like they have lost control or with a limited understanding of the steps and challenges ahead.

This article is the first in a series dedicated to the business sale process and the specific challenges of each stage. The aim is to provide entrepreneurs with guidelines to confidently navigate a transaction and focus on the strategic aspects of selling their business.

Before analyzing the key components of a business sale in detail, we must remember that time is one of the most critical factors in a transaction.

The parties involved in a transaction must have a reasonable amount of time to prepare, implement, and negotiate its key components.

Time and again, it has been observed that a lack of momentum in a transaction has negative effects on its smooth progress, often referred to as “deal fatigue.”

However, quick response times and thorough follow-ups are not only expected by the other party but are an essential part of a business sale transaction, particularly in the context of mergers, acquisitions, and business buyouts.

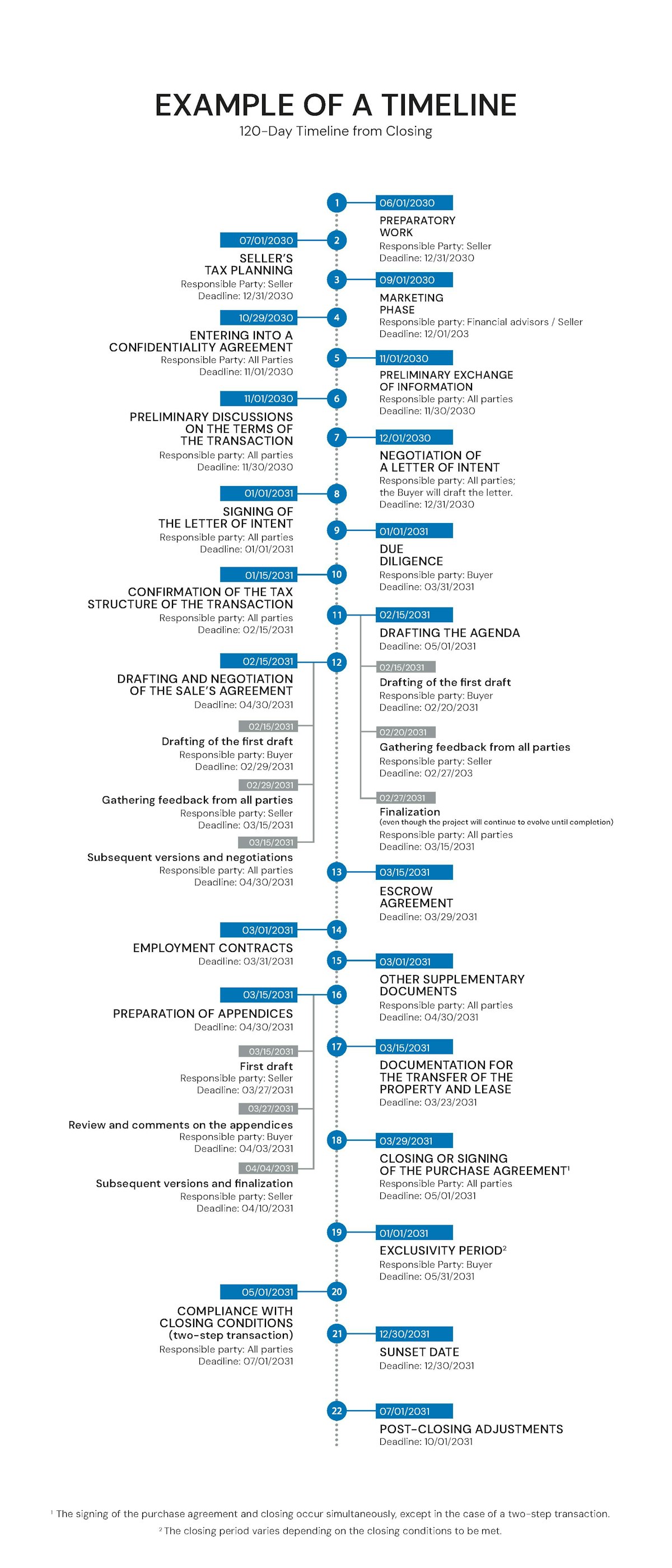

Typically, most transactions involving medium-sized businesses are closed within 60 to 150 days following the signing of a letter of intent. The overall pace of a transaction will speed up or slow down depending on economic trends, although many other factors also come into play.

Depending on its complexity (which is not necessarily proportional to its value), the number of steps required to complete a transaction may vary. However, the main stages of a sale process remain the same. Here is what a typical transaction timeline looks like:

The timeline above identifies the party typically responsible for each step. However, these responsibilities may vary depending on each transaction's specific circumstances. For example, although the buyer is usually responsible for preparing the letter of intent, an entrepreneur considering selling their business to their executives (management buy‑out) will often take the lead in drafting this document.

The timeline shown here is very linear. Just as adhering to a timeline helps ensure a smooth transaction, the parties’ flexibility regarding it also facilitates negotiations. Time can, in fact, be a powerful strategic tool, sometimes working in the buyer’s favour, sometimes in the seller’s. For example, the passage of time results in expenses for the buyer (due diligence costs, legal fees, etc.), which may prompt them to bring the transaction to a close.

The exclusivity period refers to the period during which the seller agrees to negotiate exclusively with the buyer, who will generally want it to be as long as possible. It almost always begins upon the signing of the letter of intent.

Granting an exclusivity period affects the parties’ bargaining power. Lasting between 60 and 180 days, though usually limited to 60 to 120 days, the exclusivity period will significantly influence the timeline. After all, the buyer will want to avoid finding themselves in the uncomfortable position of finalizing the transaction while the seller is free to negotiate with other potential buyers.

The due diligence period should be treated as a separate phase. However, a buyer will often use the first part of due diligence to validate the key assumptions on which they based their purchase price and payment terms. Tax and legal due diligence will usually follow subsequently.

Preparation of the closing agenda often begins fairly early in the process. Although not necessarily the standard approach, discussions surrounding this document allow the parties to have a clearer picture of the transaction’s documentary progress. Since the agenda outlines expectations and conditions required for the transaction’s completion—including solutions to issues identified during due diligence—its timely preparation also helps avoid unpleasant surprises or misunderstandings.

The closing date is usually the first day of a given month. A sale transaction generally results in a change of control, causing the target company’s fiscal year to end on the day before the transaction closes. It is therefore often best for this fiscal year-end to coincide with the end of a month to ease the company’s regular accounting activities, as well as the financial separation between the seller and the buyer.

From a tax perspective, the parties will often wish to close a transaction before a federal or provincial budget is released, in anticipation of changes that could potentially affect the net result of the transaction.

In the timeline provided, tax planning begins within the 6 months prior to the signing of the letter of intent. However, this is not an ideal scenario, as certain tax measures require preparation well in advance of the sale process.

“Although determining the most tax-efficient transaction must be done during the sale process, it is essential to review the business’s ownership structure as early as possible. This review will allow for the implementation of all necessary measures to minimize taxes at the time of sale. For example, to benefit from the capital gains deduction, establishing a profit distribution strategy may be necessary to meet certain asset tests applicable during the two-year period preceding the sale.”

- Marc-André Godard, Partner and Head of the BCF Tax Team

One of the reasons a seller wants to close the deal within a reasonably short timeframe is to preserve the transaction's confidentiality. A leak of information about a potential transaction can be detrimental to a business, such as employee demoralization and turnover, loss of clients or suppliers, and unnecessary stress for the entrepreneur who wants to protect their resources and the company's reputation.

Officially announcing the sale of a business is often the most stressful moment for a seller. That's why it's best to avoid making such an announcement while negotiations are still ongoing.

The following question is worth raising: isn’t the seller protected by the confidentiality agreement? The challenge lies in that the consequences of leaks, while unpleasant, will not, in most cases, justify conflict with the buyer, jeopardizing the transaction, and certainly not investing the necessary funds in legal action against the buyer.

The typical timeline outlined above does not include follow-ups regarding the buyer’s financing. However, thorough follow-up is advised—with the level of caution varying depending on the buyer’s profile—for any seller wishing to close the deal within the targeted timeframe.

Many entrepreneurs are surprised at how deeply involved they and their management team must be in the sale of a business. While ensuring business continuity, their availability will be heavily relied upon throughout the sale process, from due diligence through to the negotiation of key terms of the transaction.

Among the most sought-after resources, the vice-president of finance typically plays a central role. Not only will the information they oversee be necessary for due diligence, but also for analyzing and understanding the practical impacts of the financial adjustments applicable to the transaction.

When selecting the legal counsel who will assist you with your transaction, their availability and ability to act quickly are essential factors. Not only will the various parties involved in your transaction expect a timely response from them (in M&A, a callback or email response after 24 hours feels like an eternity), but you will also want to interact with your counsel on a very frequent basis (within the same day).

Furthermore, time remains the most common measure for determining the fees payable to your lawyers. An experienced M&A lawyer should be able to provide you with an estimate of the fees applicable to your transaction, especially if you are the buyer (since, generally speaking, the buyer has more control over the process), but also if you are the seller.

Once a letter of intent has been signed, they will be able to provide a more accurate estimate, as the terms of the transaction will be more clearly defined. Since some variables may only become clear during the course of a transaction, a budget estimate will include certain contingencies, but your counsel should provide you with a budget that accounts for the usual uncertainties associated with a transaction.

One of the very first questions that come up when considering selling a business is: Is this the right time to sell my business?

Christine Pouliot, Vice President and Managing Partner for Québec and Eastern Canada at PwC Canada, offers the following answer:

“Although it is difficult to choose the best time to sell your business, the timing still depends on three key factors:

These three factors ought to be considered when a company’s shareholders are contemplating a sale transaction.”

If you have any questions regarding the sale of your business, please feel free to contact Nathalie Gagnon, Head of the Business Law Group, Montréal office, partner, and M&A lawyer.